When cities and teams unveil plans for shiny new stadiums, the headlines almost always focus on glitzy renderings, promises of “revitalization,” or civic pride.

The part that almost never makes the lead paragraphs is simple yet crucial: who actually pays for these facilities and why does it matter for everyday taxpayers, fans, and athletes?

In reality, “publicly funded” stadiums are rarely funded purely by taxpayers, and they almost never function as free gifts from local governments to team owners.

Instead, they are complex financial products, blending layers of public dollars, municipal debt, private investment, and league or corporate contributions. What that balance looks like in practice has huge implications for local budgets and community outcomes.

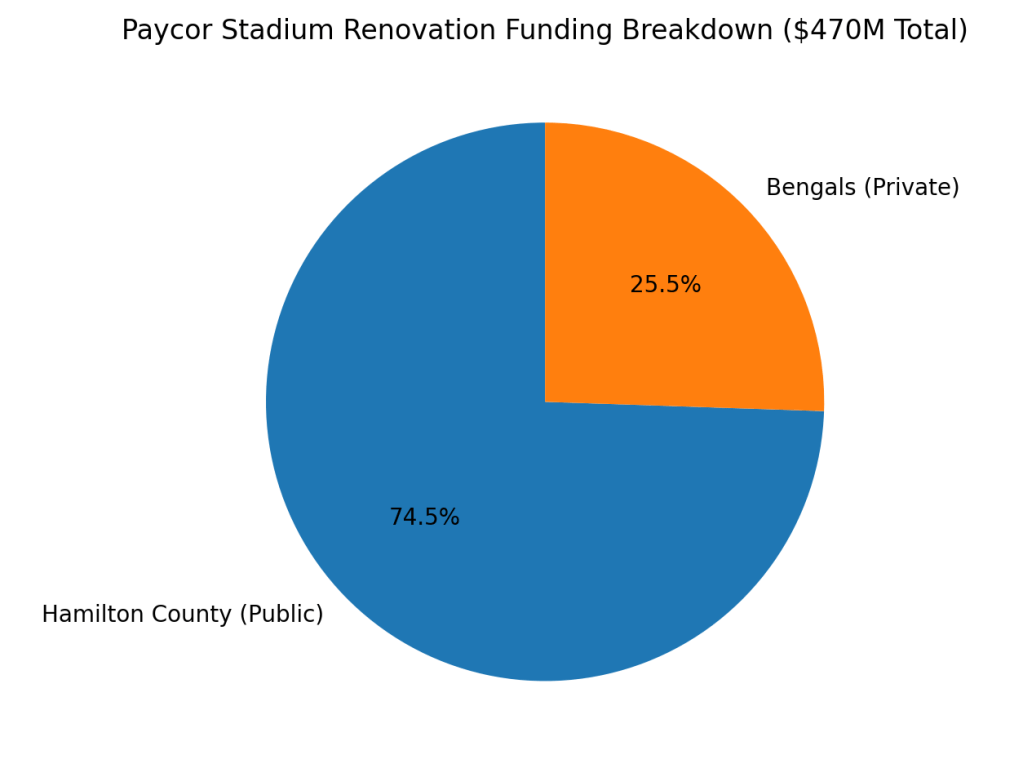

For instance, in Cincinnati, the Bengals and Hamilton County recently agreed to a tentative $470 million renovation deal for Paycor Stadium, with ~$350 million coming from the county and the team contributing ~$120 million toward upgrades like suites, concessions, and technology, a scaled-back version of a much larger vision that once approached $830 million.

Hamilton County, which owns the stadium, has spent tens of millions on maintenance and previously invested in upgrades, highlighting how stadium deals are decades-long bargaining processes, not one-off construction projects.

Just to the east in Cleveland, the Browns’ pursuit of a new $2.4 billion domed stadium has brought Ohio lawmakers into the fray.

In mid-2025, a state budget approved $600 million in public funds toward that project, drawn from dormant “unclaimed funds,” with the Haslam Sports Group and private partners responsible for the rest of the build and cost overruns.

This arrangement has already sparked controversy, not because stadiums are inherently bad, but because the use of public assets and tax dollars for privately owned facilities raises questions about public value versus private gain.

In the nation’s capital, the Washington Commanders and the District of Columbia agreed to a $3.7 billion stadium and mixed-use development at the RFK site, where the team is financing the bulk of the stadium itself, roughly $2.7 billion, while the city commits over $1 billion for infrastructure, utilities, parking, and recreation improvements.

This project, one of the most expensive in NFL history, exemplifying another trend:

Sports stadiums increasingly form the anchor for broader urban redevelopment plans, promising retail, housing, parks, and transportation upgrades.

But those municipal commitments still represent real public capital and future tax obligations.

Meanwhile, in markets like Kansas City, voter referendums and tax debates over the Chiefs’ future stadium investment have shown that even fans who love their teams can grow skeptical of pouring public resources into billion-dollar facilities, especially when infrastructure needs compete with schools, transit, traffic and public safety.

These debates aren’t isolated. They reflect a deeper shift in how cities view stadium financing.

Less as civic boons and more as long-term financial commitments with opportunity costs.

This pattern isn’t limited to one city or franchise, it’s a trend across American professional sports, where the interplay of private profits and public financing is reshaping how teams negotiate with local jurisdictions and how communities reckon with the cost of keeping a franchise in their city.

The gloss about “economic impact” rarely survives scrutiny, but the financial structure, the capital stack, tells the real story of who takes on risk and who captures value once the stadium opens.

Who Actually Pays?

Every few years, a major American sports league rolls out another billion-dollar stadium announcement accompanied by renderings, hype videos, and promises of “economic impact.”

But beneath the marketing is a financial model that matters not just to team owners and leagues, but to taxpayers, players, and fans.

The price tag of modern stadiums has climbed faster than nearly any other sports asset.

Since 2000, over $40 billion has been spent on stadium and arena construction in the U.S., and the newest generation of builds routinely sits between the $1.5 billion and $3.5 billion range.

The Titans’ Nissan Stadium redevelopment (~$2.1B), the Bills’ Highmark Stadium (~$1.7B), and Raiders’ Allegiant Stadium (~$1.9B) are another three recent examples of how far the baseline has moved.

College athletics has joined the race too. Facilities arms races across the SEC, Big Ten, and Big 12 have produced $200M–$600M football operations facilities, indoor practice fields, and athletics performance centers, financed through donations, boosters, university capital, or debt structures.

When construction costs rise, the next logical question follows:

Who pays for all of this?

Public vs Private Funding

A publicly funded stadium is almost never 100% taxpayer money.

Instead, it is a capital stack, a layered financing structure typically blending:

- City, county, or state contributions

- Municipal debt

- Tax surcharges

- Team/owner equity

- League loan programs (e.g., NFL G4/G5)

- Private revenue streams (PSLs, naming rights, sponsorships)

A publicly funded stadium is almost never 100% taxpayer money, and it’s almost never 100% privately financed either.

Instead, stadium deals are built like capital markets products: a capital stack. That stack blends city and state contributions, municipal debt, tourism or hospitality tax surcharges, team and owner equity, league loan programs such as the NFL’s G4/G5 system, and private revenue streams like naming rights, sponsorship packages, and personal seat licenses.

Each layer carries its own risk profile, repayment schedule, and political visibility, which is why stadium finance reads more like structured product design than real estate. The logic is straightforward.

Public financing reduces the upfront cost and risk exposure for ownership.

Private financing captures the downstream gains, tickets, suites, concessions, naming rights, sponsorships, non-sports event revenue, and ultimately, franchise valuation uplift. Cities take on debt.

Teams collect cash flow. Over a long enough time, one side socializes cost, the other privatizes return.

A stadium that is 60% publicly financed and 40% privately financed behaves very differently from one that is 40/60, not in headlines, but in how the project pays back over 20 to 30 years.

The higher the public share, the greater the reliance on tax revenue, hospitality surcharges, or general-obligation bonds to service debt.

The higher the private share, the greater the need for owners to monetize corporate inventory, premium seating, partnerships, clubs, suites, and naming rights, to justify capital outlay.

The blended structure also dictates who owns which revenue streams, which is ultimately where most of the negotiation happens.

Even within the same ratio, stakeholder control changes the result. A city covering 50% through municipal bonds is not the same as a tourism district covering 50% through visitor hotel taxes.

One places burden on residents; the other passes it to out-of-town visitors and event traffic.

Likewise, an ownership group financing 50% through direct equity is different from financing 50% through PSLs and naming rights, because the latter sells future revenue forward to de-risk the near term, while the former preserves upside.

From a private equity lens, stadiums resemble LBOs: levered assets with predictable cash flow, long-duration contracts, and high exit valuations.

This is also where most of the public confusion exists. To voters, the conversation focuses on whether the city “pays” for a stadium.

To ownership, the conversation focuses on who controls the revenue stack: concessions, suites, clubs, parking, PSLs, esports events, concerts, festivals, and media rights.

The political side debates cost.

The financial side debates upside.

What the Breakdown Looks Like in Practice

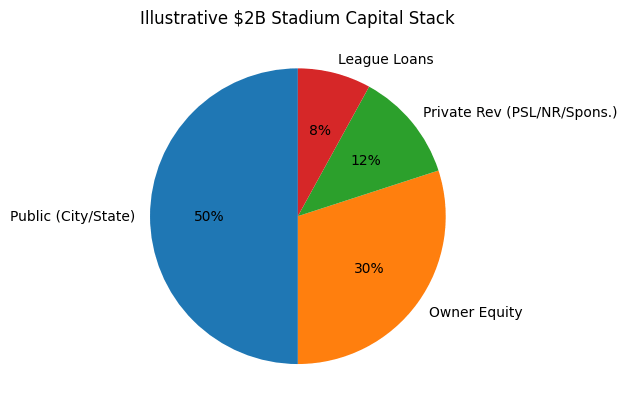

Take a hypothetical $2B NFL stadium, comparable to recent projects:

Capital Sources Breakdown:

- Government (city/state): 40–60%

- municipal bonds

- sales/hotel/rental-car tax increments

- infrastructure improvements (roads, transit, utilities)

- land transfers or abatements

- Team/Owner Equity: 20–40%

- cash/equity injection

- seat licenses (PSLs)

- luxury suite deposits

- strategic partners

- Private Revenue Financing: 10–25%

- naming rights

- sponsorships

- media/partnership revenues

- long-term vendor contracts (e.g., food & bev)

- League: 5–15%

- G4/G5 loans (NFL)

- equivalent assistance mechanisms (NBA/NHL/MLB varies)

- Federal Subsidies (implicit):

- tax-exempt bond interest

- depreciation models

- accelerated write-offs

- opportunity zone advantages (in select cases)

On paper, this looks cooperative. In reality, two things matter more:

- Who services the debt?

- Who owns the revenue streams?

From a capital markets perspective, stadium construction isn’t truly a civic good, it’s a leveraged real estate asset wrapped in sports branding.

When teams pursue new venues, the structure resembles a traditional capital stack: public participation via municipal bonds and hospitality taxes, private equity from owners, structured revenues from naming rights and PSLs, and league assistance through loan programs like the NFL’s G4/G5 system.

Federal tax exemptions sit quietly at the bottom, lowering capital costs through tax-free bond interest and accelerated depreciation.

On paper, it looks cooperative. In practice, the more important questions are who carries the debt and who captures the cash flow.

A modern $2B NFL stadium typically sees 40–60% financed by cities or states through bonds and tourism taxes, another 20–40% through owner equity and private investors, and a final tranche from leagues and naming rights.

The public funds service debt while the private funds monetize suites, concessions, sponsorships, and seat licenses. That’s the core design that allows stadiums to be publicly financed but privately monetized.

Debt loads sit on civic balance sheets. Revenue sits on income statements.

The economic rationale is clear.

New stadiums increase EBITDA through premium seating, expanded corporate inventory, upgraded sponsorship packages, and non-sports event revenue.

Because major U.S. sports teams trade at financial multiples, NFL teams often at 8–12× EBITDA, NBA slightly higher at 10–14× incremental facility revenue translates directly into valuation uplift.

If a stadium adds $80M in annual EBITDA, a simple 10× multiple yields an $800M valuation gain, which can exceed the owner’s total equity contribution.

Public dollars reduce risk. Private dollars capture return.

The carry trade is clean.

The prize isn’t simply retaining a team, it’s avoiding the negative optics of losing one. The returns, however, continue to accrue to ownership.

Stadium economics remain one of the cleanest examples of privatized gains and socialized costs in modern American capital markets.

Hidden Cost #1: Taxpayer Exposure + Bond Risk

Bonds don’t care about records. If the stadium underperforms, taxpayers still owe the debt.

Cities like St. Louis and Oakland were still servicing stadium/arena debt after teams left entirely, a scenario where public money built an appreciating asset that then relocated to a different market.

This dynamic isn’t small. Stadium bonds can extend 20, 30, sometimes 40 years beyond ribbon cutting.

Hidden Cost #2: Opportunity Cost of Capital

When a city funds a stadium, it isn’t just writing a check, it’s committing to what it won’t fund instead.

Economists like J.C. Bradbury (Kennesaw State) and Victor Matheson (Holy Cross) estimate that stadiums rarely deliver sustained local GDP growth, meaning public ROI often underperforms:

- Jobs created are temporary (construction, event staffing)

- Spending is substitutional (entertainment dollars shift from elsewhere)

- Profitable revenue streams sit with the team, not the city

From a civic standpoint, this means stadiums often function closer to consumption goods than infrastructure.

Enjoy Reading How Money Works In Sports?

Take a break from the action and Buy The APSM $100 million –> $35 million Net Contract Report.

The Report Includes:

- In-depth contract structure analysis

- Taxes, agent fees, and escrow modeling

- Endorsement and bonus impact scenarios

- Investment & wealth retention strategies

- Real-world case studies of player earnings vs take-home

Everything you need to understand how multi-million dollar contracts translate into actual wealth

and how to avoid common

financial pitfalls in pro sports.

You may just end up learning

a thing or two you can apply

to your own finances.

Bet against time, not your future.

Why Owners Push for Public Money

From a finance perspective, stadium deals make perfect sense, even if the public messaging around them is muddy.

Public dollars reduce risk, increase franchise value, and free private capital for competitive spending. The result isn’t ideological, it’s structural.

When cities or states cover a meaningful portion of stadium financing, they effectively de-risk one of the most capital-intensive investments a franchise can make.

Debt is amortized over decades, interest costs are diluted through municipal instruments rather than private credit, and owners avoid tying up capital that could be deployed elsewhere in the enterprise.

Reduced capital burden has two immediate consequences:

Franchise Valuations Increase

Across modern sports transactions, the most reliable valuation lever isn’t winning, star players, or brand, it’s infrastructure.

A new stadium (or even redeveloped), can tack hundreds of millions to more than a billion dollars onto a team’s enterprise value.

That uplift accrues entirely to the ownership group, not to the jurisdiction that helped fund it.

The city pays for an amenity; the owner gets an appreciating asset that can be sold at a premium.

Private Capital is Redeployed into Players and Performance.

When owners don’t have to finance stadium construction out-of-pocket, the cash preserved can be redirected toward rosters, payroll, scouting, analytics, sports science, NIL, or broader competitive infrastructure.

In a league like the NFL or MLB, where competitive spending is a function of both cash flow and risk tolerance, public financing can indirectly shape roster outcomes.

Fans see the effect in the form of better facilities, more aggressive payroll posture, and more ambitious front office strategies.

Cities rarely “lose” franchises because fans don’t care, they lose because the financial ecosystem of stadium funding is sharpened by competition. In a world where a new stadium can add $1B+ in valuation uplift, league approval becomes a form of M&A transaction.

Nobody relocates for nostalgia, they relocate for asset appreciation, revenue optionality, and control of real estate.

For jurisdictions, the calculus is different. They chase civic pride, tourism, cultural signaling, and downstream economic spillover, but the valuation upside is privatized.

The city doesn’t own equity in the team, the real estate, or the future sale proceeds. The public absorbs cost and risk; the private entity captures appreciation. It’s not inherently unfair, it’s just structured that way.

Stadium finance isn’t about sports, it’s about capital formation, jurisdictional competition, and the transfer of financial upside from the public domain to the private ledger.

That’s why stadium negotiations always escalate toward relocation threats: the leverage exists because the financial reward of winning the negotiation is measurable, while the cost of losing a team is emotional.

Stadiums as Leverage, Politics, and Asset Appreciation

The NFL is the cleanest lens for understanding modern stadium economics because it blends three forces better than any other league: media rights, franchise valuation, and public bargaining power.

Renovations improve hospitality inventory (suites, clubs, field-level experiences), which in turn expands premium revenue that can support higher payrolls and more aggressive football operations.

The stadium itself is only half the negotiation. The real prize for jurisdictions is the surrounding redevelopment, mixed-use real estate, and long-term property value.

In modern NFL economics, stadiums are no longer standalone venues, they are anchors for retail, residential, hotel, and entertainment districts, and those are financed through a blend of public infrastructure, tax abatements, and private capital.

College Facilities: The Quiet Billion-Dollar Race

College sports don’t frame their construction projects as “stadiums,” but they represent one of the most aggressive facility races in American sports finance.

Over the last decade, the SEC alone has deployed $4B+ in facility spending: indoor practice facilities, player lounges, NIL-support centers, academic hubs, nutrition programs, and performance labs.

These aren’t fan amenities, they are recruiting assets, and in the NIL era, recruiting is capital allocation.

The financing structure mirrors professional stadiums more than people realize.

Boosters act like private equity, injecting donor capital to increase program competitiveness.

University capital functions like municipal financing, supporting long-term projects with multi-decade ROI horizons.

Naming rights in college sports are effectively sponsorship deals, where brands pay for visibility, community positioning, and alumni access.

Conference media rights serve as the college equivalent of league revenue sharing, the SEC, Big Ten, and Big 12 distribute cash flows that justify further investment.

The ROI on college facilities is indirect but real. Winning recruits increases winning seasons, which boosts media exposure, playoff appearances, and donor momentum.

In a post-Playoff expansion era, that flywheel intensifies:

facilities → recruiting → winning → media rights → donor cycles.

The result is a form of infrastructure competition that resembles arms races in tech, not amateur athletics.

Universities don’t issue public bond measures the way cities do, but public money still finds its way into these projects through state allocations, tax-engineered donations, and land usage.

The difference is that voters don’t get a ballot, they get a press release.

How Fans & Athletes Actually Pay

Stadium economics don’t end once construction is finished, that’s when the second phase begins.

Fans pay directly through tickets, PSLs, parking fees, concessions, and merchandise, all priced at premiums that reflect the cost of the venue.

Naming rights create an additional pass-through mechanism: companies don’t buy stadium naming rights out of goodwill, they bake that sponsorship expense into product pricing and marketing budgets. Indirectly, fans pay again.

Taxpayers participate more discreetly. Municipal taxes, hotel taxes, rental car surcharges, sales tax adjustments, and public debt servicing continue for decades.

Even residents who never attend a game may fund a stadium through economic externalities.

In event-heavy cities like Vegas, Nashville, New Orleans, stadium economics can drive local inflation in hospitality and transportation.

Athletes enter the loop through valuations. Higher team valuations raise payroll capacity in leagues with soft caps (NBA) or revenue sharing mechanisms (NFL, MLB).

Stadiums produce premium seating, sponsorship inventory, and hospitality assets, all of which increase total revenue and revenue is the definitional input for salary caps and competitive payroll.

When economists argue stadiums don’t drive economic growth, they’re talking about cities. When players argue new stadiums benefit careers, they’re talking about team-level economics, which are very real.

In the aggregate, stadium finance becomes a pass-through ecosystem:

The city subsidizes construction.

Fans fund operations.

Players capture competitive payroll. Owners lock in valuation growth.

It’s not exploitative, it’s just misunderstood. The key question isn’t whether stadiums create value.

It’s who captures it.

Actionable Questions For Future Stadium Deals

For fans, voters, and policymakers, every stadium proposal comes down to a set of financial questions that rarely appear in the press release:

- Who owns the revenue streams? Premium revenue, naming rights, and PSLs often determine whether the deal is team or city-friendly

- Who services the debt? A city paying bond principal + interest for 30 years is very different from a team amortizing private financing.

- What is the public/private split, in percentage and in structure? $500M in infrastructure improvements can be more impactful than $500M in direct stadium cash.

- What is the exit risk? Teams use relocation as leverage because valuations depend on optionality, not geography.

- Does the public share in upside or just cost? Green Bay is the rare example of community upside; most markets see one-way benefit flows.

- What’s the lifecycle timeline? Most stadiums undergo major renovations by year 12–15, well before bonds mature.

- Is the ROI financial, cultural, or political? The worst outcomes are when a city pays for cultural ROI while ownership captures financial ROI.

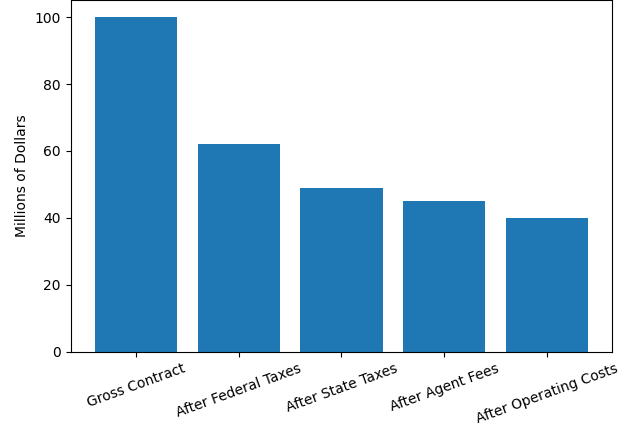

Why a $100M Pro Contract Often Nets Only $35M–$55M

Enjoy Reading How

Money Works In Sports?

The APSM Net Contract Report provides deeper analysis into the real world of money in sports and why headlines figures are gross.

The Report Includes:

- In-depth contract structure analysis

- Taxes, agent fees, and escrow modeling

- Endorsement and bonus impact scenarios

- Investment & wealth retention strategies

- Real-world case studies of player earnings vs take-home

(Example Graphic from the Report)

This report has everything you need to understand how multi-million dollar contracts translate into actual wealth and how to avoid common financial pitfalls in pro sports.

Bet against time, not your future.

Next Reads

- Inside the Bengals’ $470 Million Stadium Renovation Deal

- The Actual Costs of the Cleveland Browns’ New Stadium Deal

- Inside the Chiefs’ Push for a New Stadium Location

- Inside the Washington Commanders’ Stadium Fight

- Why Sports Tickets are More Expensive than Ever

Credits

Author: Aidan Anderson

Research & Analysis: Apostle Sports Media LLC

Sources: ESPN, The Athletic, Brookings Institution, J.C. Bradbury, Victor Matheson, Sports Business Journal, APSM Proprietary Analysis

Featured Image: Public Domain / Instagram

Disclaimer: This article contains general financial information for educational purposes and does not constitute professional advice.